By George Abonyi and David Abonyi, April 16, 2026

Canada is facing a pivotal moment in a turbulent world where traditional economic relations are shifting. Its response requires a clear external economic strategy, including diversification of relations. But without careful analysis, such diversification risks being ineffective – or even counterproductive.

A key priority should be the expansion and enhancement of Canada’s Indo-Pacific Strategy (IPS), which we have previously addressed. This discussion instead focuses on Canada’s two other priorities – China and Europe – as well as emerging economic corridors reshaping the world’s economic geography.

China, the world’s second-largest economy, is a major export market and a key player in global value chains and Asian production networks, with a critical position in the Indo-Pacific. It offers significant opportunities, but misreading China’s economic realities could have costly consequences for Canada’s economy, its engagement with ASEAN partners, and with the broader Indo-Pacific region.

The European Union (EU), the world’s third-largest economy, offers high-income customers and standards-based opportunities for Canadian firms. However, its economy faces fundamental challenges and uncertain prospects, requiring a realistic assessment of structural fragilities and ongoing policy uncertainty.

Emerging economic corridors are reshaping global trade, investment, and the broader framework for economic co-operation. While Canada is not a direct participant in most of them, their development has important strategic implications and presents new opportunities for creative economic diversification.

Economic diversification challenge

The global economic and geopolitical order is undergoing a profound transformation, marked by instability, complexity, and interdependence. Disruptions are no longer discrete events but continuous conditions. As Emery and Trist noted in their 1965 Human Relations article, such environments are “turbulent” – an insight that resonates strongly today. Modern shocks, whether technological or geopolitical, now arrive faster, spread further, and increasingly difficult to predict.

Technological innovation is a key driver of change. Artificial intelligence (AI) is reshaping industries, labour markets, and consumer behaviour, with both productivity gains and disruptive social consequences. Geoeconomics is another force, exemplified for Canada by recent United States policy, where governments are increasingly displacing firms as key decision-makers across markets ranging from medical supplies to energy, semiconductors, and agriculture. In short, Canada faces a world in which traditional economic patterns, rules and relationships are being rewritten.

In response, Canada must address long-standing economic challenges documented by institutions such as the C.D. Howe Institute and RBC Economics, and reports in the Financial Times, as well as more targeted studies from the Macdonald-Laurier Institute highlighting issues like interprovincial trade barriers, capital investment, and tax reform. Parliamentary studies have similarly underscored Canada’s innovation and productivity gaps.

Externally, the US, the world’s most dynamic and powerful economy, remains the anchor of Canada’s prosperity and security. While that relationship will remain central, a turbulent world requires an economic strategy includes diversification but does not distance Canada from the United States. Instead, it should expand choices, strengthen resilience, and enhance strategic flexibility amid growing uncertainty.

Effective diversification requires rigorous analysis of the global economy and Canada’s role within it. Lessons from past efforts, such as former Prime Minister Pierre Trudeau’s “Third Option” initiative, illustrate the perils of diversification without clear-eyed analytical grounding.

Understanding the China challenge

Canada’s Indo-Pacific Strategy (IPS) rightly positions China as a central yet complex economic and geopolitical actor. Engagement with China remains necessary. It is a major export market and plays a pivotal role in global value chains, anchoring Asian production networks and a rapidly expanding regional consumer market.

However, engagement based on flawed assumptions about China’s economic trajectory carries serious risks. China’s economy is more fragile, uncertain, and more externally disruptive than headline growth figures imply. Misdiagnosis could have significant consequences for Canada.

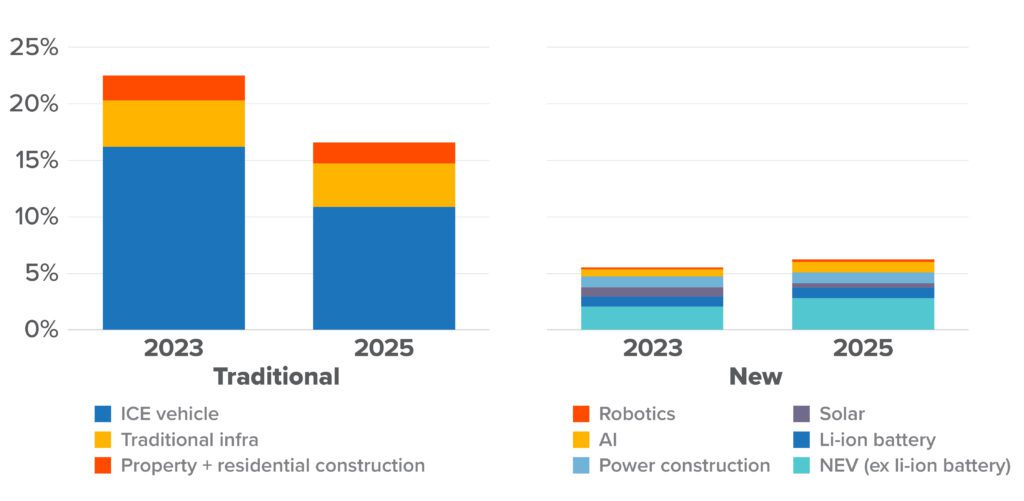

China’s official narrative emphasizes a smooth transition from traditional growth engines such as property and real estate, infrastructure, and conventional manufacturing toward “new” high-technology industries such as electric vehicles, batteries, clean energy, artificial intelligence, and robotics. Yet the data point to a widening gap between narrative and performance.

Between 2023 and 2025, output from traditional sectors fell by roughly six percentage points of GDP, while new industries added less than one (see Figure 1). The old engines are shrinking faster than the new ones are growing. Even optimistic projections suggest the latter would need implausibly rapid expansion to achieve a GDP growth target of say 5 per cent in the next five years. Moreover, these newer sectors generate fewer jobs and weaker consumer demand.

Figure 1: Estimated upstream and downstream economic output of traditional and “new” industrial sectors, 2023 and 2025

Source: The Rhodium Group

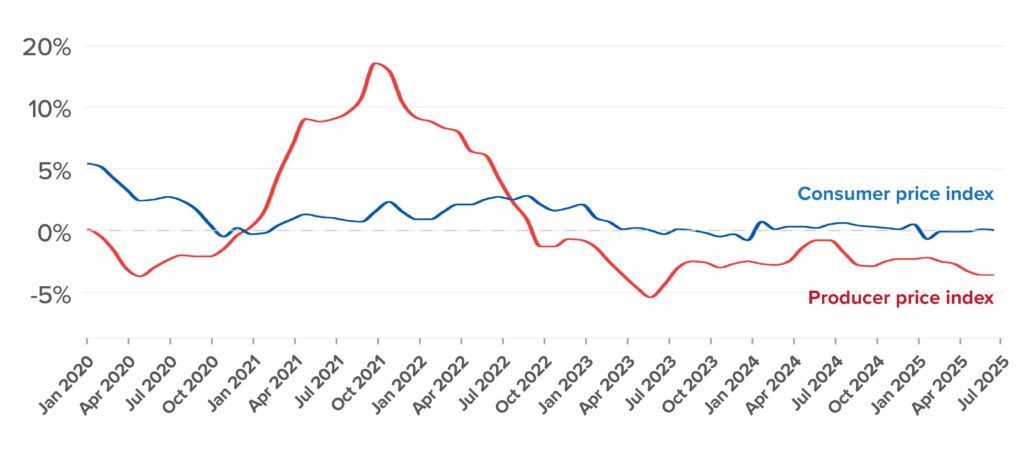

Furthermore, China’s economy is characterized by persistent overproduction in sectors such as EVs and clean energy, coupled with chronic under consumption. The problem is structural, reflecting industrial policy embedded in instruments such as the Catalog of Industrial Guidance, which steers capital, credit, and administrative support toward designated priority sectors under successive Five-Year Plans.

This has led to rapid capacity expansion and intense price competition in priority sectors, disconnected from domestic demand conditions. The result is deflationary pressure reflected in both producer and consumer price indices (see Figure 2), downward pressure on wages and employment, and rising financial stress as capital is locked into unproductive investment for example in inventory and excess capacity.

Figure 2: China’s producer and consumer price indices (year over year change, 2020–25)

Source: CSIS 2025

In the face of these challenges, China has had little success increasing domestic consumption to create the necessary demand in response to overproduction. Reducing excess capacity by allowing non-viable loss-making firms to fail is socially and politically risky, as China is faced with significant and rising rural underemployment, and youth unemployment near 20 per cent.

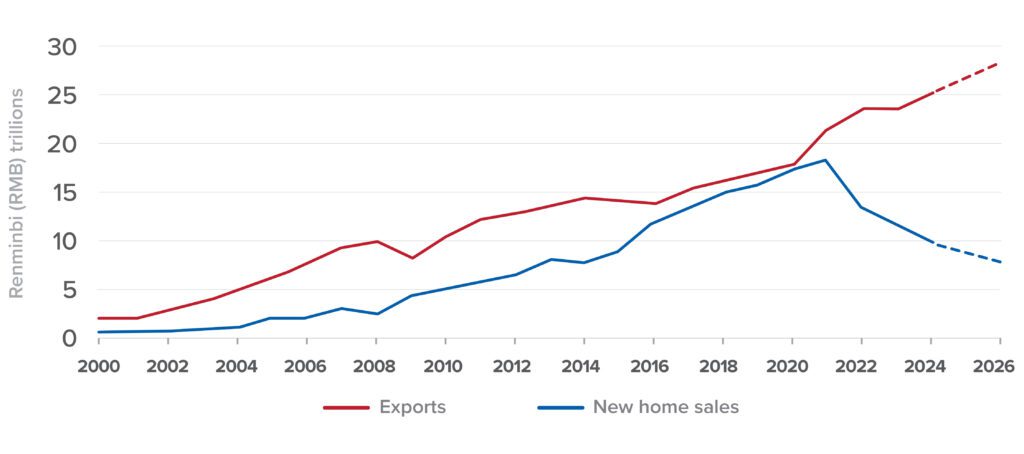

The result is an economy increasingly dependent on exports to meet politically determined growth targets, and to stave off even deeper and wider deflation. China’s trade surplus reached a record US$1.2 trillion in 2025, nearly three times its 2019 level. This surplus is not a sign of domestic strength but of structural imbalance: production continues to surge while consumption remains weak. The IMF’s managing director recently warned Beijing that such surpluses are unsustainable and heighten exposure to trade restrictions and external shocks.

The relationship between dependence on exports and weakening domestic demand is summarized by Nomura as the “big divide” (see Figure 3), with rapidly collapsing property sector or new home sales as a proxy for wider and deeper weaking of domestic demand.

Figure 3: “The big divide”: China’s export dependency amid weakening domestic demand

Source: Nomura Connects 2025

The policy and operational implications for Canada are both direct and indirect. As the US and EU tighten restrictions on imports from China, Canada is at risk from increasing pressure to become a secondary destination for redirected Chinese exports. China’s state-supported overcapacity in areas such as EVs, batteries, and clean energy directly affect sectors Canada has identified as strategic priorities. Canada must be ready for hard negotiations, for example on follow-up to the presently agreed EV-related limited import quotas as China’s export pressures on Canada increase. The difficult EU experience with Chinese EVs is a clear illustration. In addition, China’s new restrictions on technology imports and heightened emphasis on domestic substitution limit prospects for expected Canadian high-value exports in advanced sectors, such as green technology.

Association of Southeast Asian Nations (ASEAN) economies, central to Canada’s Indo-Pacific Strategy, are under considerable pressure, becoming the leading recipient of redirected Chinese exports. While there are benefits from China’s investment in regional supply chain integration, there are also increasing risks to ASEAN domestic economies. This is reflected in factory closures in vulnerable industries, for example in Indonesia and Thailand.

Yet, these economic disruptions can create novel opportunities for Canada – ASEAN collaboration, as both look to diversify traditional economic linkages. For example, the ASEAN Digital Economy Framework Agreement (DEFA) is projected to increase the value of region’s digital economy to US$2 trillion by 2030, providing significant scope for Canada’s exports and partnerships in digital technology and services. Similarly, Invest ASEAN, an investment promotion platform to be launched this year with initial focus on the biofuel supply chain, also a Canadian policy priority, creates new opportunities for co-operation.

Engagement with China remains strategically necessary, with significant scope. But it must be well thought out, targeted, and grounded in rigorous analysis as the basis for effective policy direction and practical initiatives. Misreading China’s economic realities will not serve well Canada’s interests for engagement with China, with ASEAN partners, and with the broader Indo-Pacific region.

Europe at a crossroads

The European Union offers a large market with high-income customers, strong regulatory institutions, deep capital pools, and standards-based trade. Yet closer analysis reveals a slow-growth economy, with mounting structural and sector-specific fragilities and risks.

As Europe’s largest economy and the world’s fourth-largest after the US, China, and Japan, Germany has long served as the continent’s industrial engine. That engine is now sputtering. Germany has been in a prolonged manufacturing slump since 2022. Its export-driven model, which has anchored European growth, has faltered under the combined weight of weak global demand, a strong Euro, intensifying Chinese competition, US tariffs, and higher domestic costs.

Energy-intensive sectors, particularly key chemicals and autos, were especially hard hit by soaring gas costs, following loss of inexpensive Russian supplies. The EU’s net zero policy is seen further constraining German and European manufacturing industries. Leading companies have begun shifting production abroad. BASF, one of the world’s largest chemical companies, is pivoting investment toward the US and Asia. Volkswagen is closing German factories for the first time in its history. By late 2024, German industrial output stood roughly 10 percentage points below pre-pandemic levels, a sharper contraction than in most of the euro area, dragging down production in neighbouring economies from Italy to France.

This is not a cyclical dip; it reflects deeper structural stress. Planned government spending on infrastructure and defence is unlikely to spark meaningful recovery without fundamental reforms. Weakness in Germany is weakness in Europe as a whole (see Figure 4).

Figure 4: Germany: Europe’s sputtering engine

Source: CEPR 2025. Note: all data are seasonally adjusted and in 3-term moving averages. Last observation: November 2024.

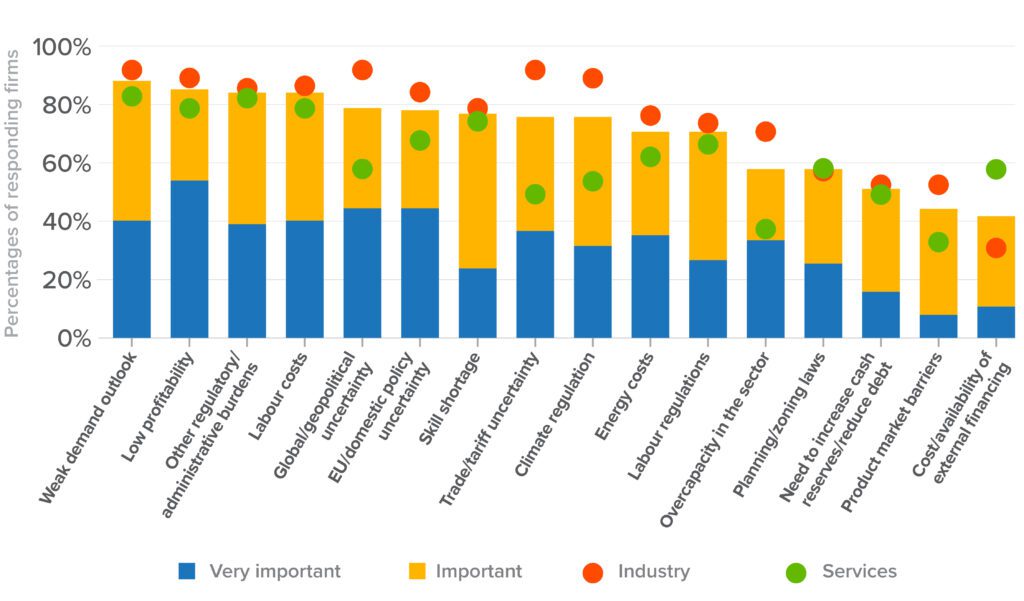

Reflecting Germany’s challenges, the broader European outlook remains subdued. Across Europe, aging populations, stagnant productivity, and inflexible labour market institutions constrain growth. Surveys of euro-area firms show expectations of near-stagnant business investment over the next three years, with many companies planning to expand outside the euro area rather than within it. Weak demand is cited by nearly nine out of ten firms as the principal constraint on investment, followed closely by low profitability, regulatory burdens, and labour costs (see Figure 5).

Figure 5: Investment pessimism of euro-area firms

Source: European Central Bank 2025

Demographics compound the challenge. Europe’s aging population and rising dependency ratio constrain labour supply and productivity growth. Long-term projections show slowing labour-force expansion across much of the continent. Closing the productivity gap with the United States would require Europe to roughly double its growth rate. This requires sweeping structural reforms, including addressing rigid labour markets, and significant capital mobilization.

A 2024 report, led by former European Central Bank President Mario Draghi, characterized Europe’s productivity gap with the United States as “existential,” calling for significant investment, regulatory reform, and deeper capital-market integration. In 2026, Draghi no longer feels this is sufficient, calling for fundamental institutional reform.

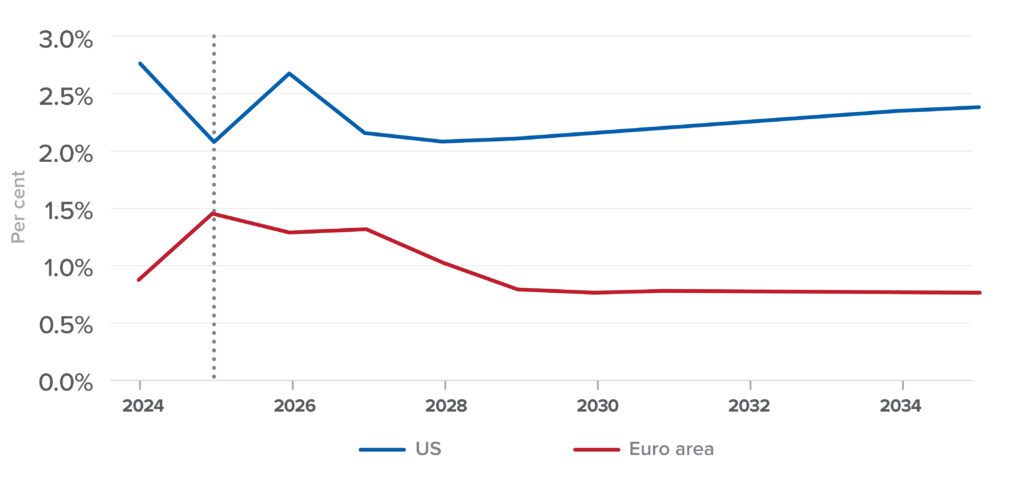

Meanwhile, Europe faces intensifying external competition. Chinese firms are capturing export market share in sectors once dominated by Germany, including autos, industrial machinery, and chemicals. At the same time, US industrial policy and digital leadership attract European investment. Some analysts warn that without structural renewal, Europe risks becoming a “dual economic colony,” industrially dominated by China, and digitally by the US. The widening growth gap between Europe and the US captures the challenge (see Figure 6).

Figure 6: Estimated GDP growth of the euro area and the US

Source: S&P Global 2026

For Canadian enterprises, sector-specific constraints also shape the risk landscape, particularly for smaller firms. European appetite for Canadian LNG may be crisis-driven rather than structurally stable. The uncertainty in Europe’s energy market is reflected in a recent statement by the German minister questioning the EU’s net zero policy, while at the same time Germany’s influential renewable energy industry calls present policy “incoherent” in the face of significant challenges.

Agri-food exports face steep regulatory barriers, including stringent sanitary and sustainability mandates, that raise compliance costs and limit scale. In technology, regulatory frameworks such as the General Data Protection Regulation (GDPR), the EU Artificial Intelligence Act, and digital sovereignty policies, create a high-cost, low-scale environment. For manufacturing, subsidies favouring local producers and domestic value-added, and fragmented markets, increase administrative complexity and operating costs.

Europe offers substantial opportunities for Canadian firms. It is not in crisis, but it is in fundamental transition with clear risks, and uncertain outcomes. Effective engagement therefore requires realistic assessment of structural fragilities and geoeconomic challenges of an economy under significant strain.

Emerging global economic corridors

Global trade is projected to expand by 30 to 40 per cent reaching $42 trillion to $45 trillion by 2035. This growth, however, is unlikely to be evenly distributed. A new generation of economic corridors is rewiring the global economy by integrating ports, railways, pipelines, energy grids, and digital networks into coordinated transnational systems. These corridors are redefining how trade, investment, energy, capital, and data move across borders, while also reshaping the geography and institutional framework of international economic co-operation. A significant share of future trade growth is expected to be concentrated along these emerging corridors.

Canada is geographically removed from most of these initiatives, which largely seek to connect Asia, Europe, and the Middle East. Nevertheless, their evolution carries important strategic implications for Canada’s long-term position in the global economy. The examples below illustrate the scale, scope, and potential impact of selected corridors now under development.

The India–Middle East–Europe Corridor (IMEC) is among the most ambitious and geopolitically complex of these initiatives (see Figure 7). Announced in 2023 at the G20 Summit in Delhi, it is a proposed transcontinental trade and infrastructure network designed to strengthen economic connectivity between India, the Middle East, and Europe. IMEC rests on three core pillars. An integrated transportation infrastructure links rail and maritime shipping, including major port hubs. Energy connectivity involves pipelines and electricity grid interconnections. Digital connectivity through fiber-optic cables provides cross-border data infrastructure. Overall, IMEC is intended to reduce transit times, lower transportation costs, improve supply-chain reliability, expand market access, and enhance energy and resource security across three major economic regions.

Figure 7: IMEC: Connecting India and Europe via the Middle East

Source: GIS Reports Online 2025

The Vertical (Gas) Corridor, anchored in the Eastern Mediterranean, is a developing network of pipelines, LNG terminals, electricity interconnectors, and transmission grids from Mediterranean entry points through the Balkans into Central, Eastern, and Southeastern Europe, including Ukraine. Its primary objective is to integrate regional energy markets and diversify supply sources and routes, including for North American LNG exports to Europe. Although initially focused on natural gas, the infrastructure is expected to be adaptable for hydrogen transport, positioning the corridor to support the longer-term transition to low-carbon energy systems

The Middle Corridor, also known as the Trans-Caspian International Transport Route, seeks to strengthen Europe–Asia connectivity, by establishing an alternative multimodal trade route linking China to Europe through Central Asia and the South Caucasus, via Kazakhstan, Azerbaijan, Georgia, and Turkey. Its strategic importance has increased as governments and firms seek to diversify supply chains, bypassing the conflict zones of Russia and Iran.

The Zangezur Corridor facilitated by the US, is a proposed transport and logistics route involving Azerbaijan and Armenia, that would further enhance connectivity between Europe and Asia and reinforce the Middle Corridor. Reportedly structured as a long-term US lease arrangement, the initiative signals a broader effort by Washington to influence the geoeconomic landscape of Eurasia through infrastructure development and transit governance.

Canada lies outside most emerging corridors. But their implications for Canadian trade and investment are significant. Expanded connectivity between Europe, the Middle East, and Asia, as with IMEC, could create new opportunities for Canadian exports, including agriculture, critical minerals, energy, and advanced manufactured goods. Similarly, the Vertical Corridor presents opportunities for exporting North American (as currently planned, mostly US) LNG to Europe and, in the future, also green hydrogen. This can provide opportunities for creative positioning of Canada, particularly for green hydrogen exports. Canadian firms could also participate in extensive corridor developments through engineering services, infrastructure construction, logistics, project finance, and energy-transition technologies.

A comprehensive and practical policy framework is needed to take advantage of opportunities offered by emerging economic corridors. This should include a focused corridor-oriented trade and investment strategy, closer alignment of relevant federal and provincial infrastructure priorities, and targeted diplomatic engagement and deeper commercial partnerships with corridor countries.

Without a coherent economic corridor policy framework that guides proactive and strategically coordinated action, Canada risks being marginalized as the geography of global trade and investment is reconfigured around emerging economic corridors.

Informed Strategic Repositioning

Canada’s economic diversification is a strategic imperative. It is not a move away from traditional partners but a pathway to resilience and strategic agility. This must be guided by continuous, rigorous, and evidence-based assessment of global economic dynamics. The lessons of China, Europe, and emerging economic corridors underline the urgency and necessity of disciplined, informed, and strategic decision-making that can point to new policy directions and practical initiatives.

In a world of technological disruption, geoeconomic competition, and structural economic shifts, Canada’s diversification strategy must be anchored in empirically grounded, rigorous analysis and continuous reassessment of assumptions about the global economy and Canada’s role within it. This, in turn, requires new types of tools and frameworks to help public policy makers and firms navigate complexity and uncertainty in turbulent times.

As Mark Twain famously supposed to have observed, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.” In a turbulent world, Canada cannot afford to be certain about the wrong things.

George Abonyi is a senior research fellow and visiting professor at the Sasin School of Management of Chulalongkorn University and senior adviser to the Fiscal Policy Research Institute, affiliated with the Ministry of Finance, Royal Thai Government.

David Abonyi is founder and CEO of Lomtara, member of the advisory board of SUSTAINISM, and director of the project “Strengthening Thai-Canada Business Linkages,” originally an initiative of the Thailand Economic Co-operation Foundation in Bangkok.

This article is significantly expanded from a previous article originally published in The Hill Times in February 2026.