Deficit spending and ultra-low interest rates are intended to stimulate the economy, writes Cross. But the trouble is that “tomorrow eventually becomes today” and this time we will lack the policy tools to rescue the global economy

OTTAWA, Nov. 30, 2016 – Governments addicted to stimulus have us headed for the next financial crisis while relinquishing the levers they will need to pull us back from the brink this time.

Macdonald-Laurier Institute Munk Senior Fellow Philip Cross, in a new paper, warns that governments are risking disaster by continuing with stimulus efforts that began during the recession of 2008.

Deficit spending, ultra-low interest rates, and other short-term stimulative measures threaten to aggravate the global financial turmoil they were originally designed to redress.

“Continuing on the present course will sow the seeds of the next crisis while depriving policy-makers of the tools they used in 2008 with which to stave off another financial crisis”, writes Cross.

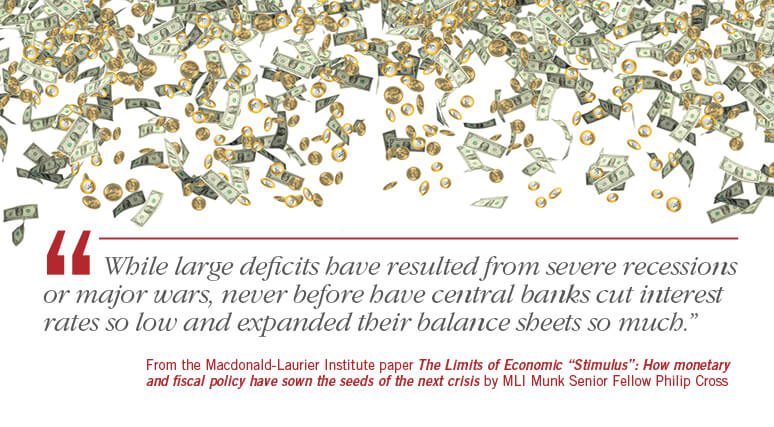

To read the full paper, titled “The Limits of Economic “Stimulus”: How monetary and fiscal policy have sown the seeds of the next crisis”, click here.

When the financial crisis in the US erupted in full force with the bankruptcy of Lehman Brothers in September 2008, it threatened to engulf the world in a depression. Almost all economic analysts agreed on the need to adopt extraordinary monetary and fiscal stimulus.

However, few of those analysts imagined such stimulus would be maintained — and even augmented – nine years after the onset of the crisis. Increasingly, Western governments, including Canada, are using stimulative monetary and fiscal policies to address persistently slow growth.

“Continuing on the present course will sow the seeds of the next crisis while depriving policy-makers of the tools they used in 2008 with which to stave off another financial crisis” -Philip Cross

Cross’s paper argues that policy-makers should reverse this experiment of monetary and fiscal policies aimed at short-term stimulus. The cost to growth of this reversal in the short-term may be minimal since the stimulative impact of maintaining these policies has waned as interest rates approached the zero bound and as government debt accumulated. For all advanced economies real GDP growth averaged 2.9 percent from 2005-2007. Since then, it has averaged 0.9 percent.

Cross points out that low interest rates have encouraged governments to delay structural economic reforms, they depress savings and therefore investment, they undermine the stability of financial institutions, and they encourage asset price bubbles and destabilizing capital flows.

Canada’s national saving rate was 10 percent before the financial crisis but it dropped to 3 percent in 2009 and has remained low, hitting 4 percent in 2015.

On the fiscal policy side, there is a limit to how much countries can borrow. And while there has been sharply-increasing government debt throughout the advanced market economies, Canadians like to think the federal government’s debt-to-GDP has them in the clear, but that’s not the case.

Including the indebtedness of the provinces puts the ratio of all government debt to GDP in Canada at only 10-13 percentage points below the levels in the US, the UK, and the euro area.

A quick look at history reveals the seeds of the next crisis are sown in the response to the previous one. The origins of the 2008 financial crisis took shape in the memory of steep capital losses in investments in Asia in the late 1990s, Cross notes. Then the US stock market in 2001 pushed Asian investors to seek the apparent security of US debt instruments, helping to fuel the bubble in the US housing market.

A quick look at history reveals the seeds of the next crisis are sown in the response to the previous one. The origins of the 2008 financial crisis took shape in the memory of steep capital losses in investments in Asia in the late 1990s, Cross notes. Then the US stock market in 2001 pushed Asian investors to seek the apparent security of US debt instruments, helping to fuel the bubble in the US housing market.

“Dealing with the fall-out of the 2007/2008 crisis resulted in nearly a decade of unprecedented monetary stimulus, the long-term consequences of which are unknown but likely to destabilize the global financial system”, says Cross.

Cross says it’s incumbent on governments to keep monetary and fiscal tools available. After all, it’s impossible to predict when or how the next crisis will strike, and they never know when they will really need them.

***

Philip Cross is a Senior Fellow with the Macdonald-Laurier Institute. He previously served as the Chief Economic Analyst for Statistics Canada, part of a 36-year career with the agency.

The Macdonald-Laurier Institute is the only non-partisan, independent national public policy think tank in Ottawa focusing on the full range of issues that fall under the jurisdiction of the federal government.

For more information, please contact Mark Brownlee, communications manager, at 613-482-8327 x105 or email at mark.brownlee@macdonaldlaurier.ca.