This article originally appeared in The Hub.

By Trevor Tombe, March 6, 2025

It is well understood that, compared to the United States, Canada’s economy lags behind. A mix of factors—including our regulatory environment, tax structures, and strained infrastructure from rail to ports to pipelines—has contributed to this gap.

Tariffs on trade between the two countries will only make it worse, putting even greater pressure on Canada’s ability to attract and retain capital.

At the same time, concerns about Canada’s own fiscal position are growing. The federal deficit remains stubbornly high, and spending continues to rise with little sign of discipline. Provinces, meanwhile, are grappling with mounting costs—especially in health care—and trade disruptions that cut into revenues. Alberta’s latest budget, for example, featured an unexpected $5.2 billion deficit this year, down from a $5.8 billion surplus last year.

But as serious as these challenges are, they remain minor compared to the fiscal crisis unfolding in the United States.

The latest projections from the Congressional Budget Office (January 2025) highlight just how dire the U.S. situation has become. The country is on track for a 10-year deficit of $21.1 trillion. With GDP projected at $373.2 trillion, that puts the deficit at 5.8 percent of GDP. By 2036, interest payments alone will climb to 4.1 percent of GDP. If Canada faced a comparable interest burden today, it would amount to roughly $130 billion—more than double what we currently pay.

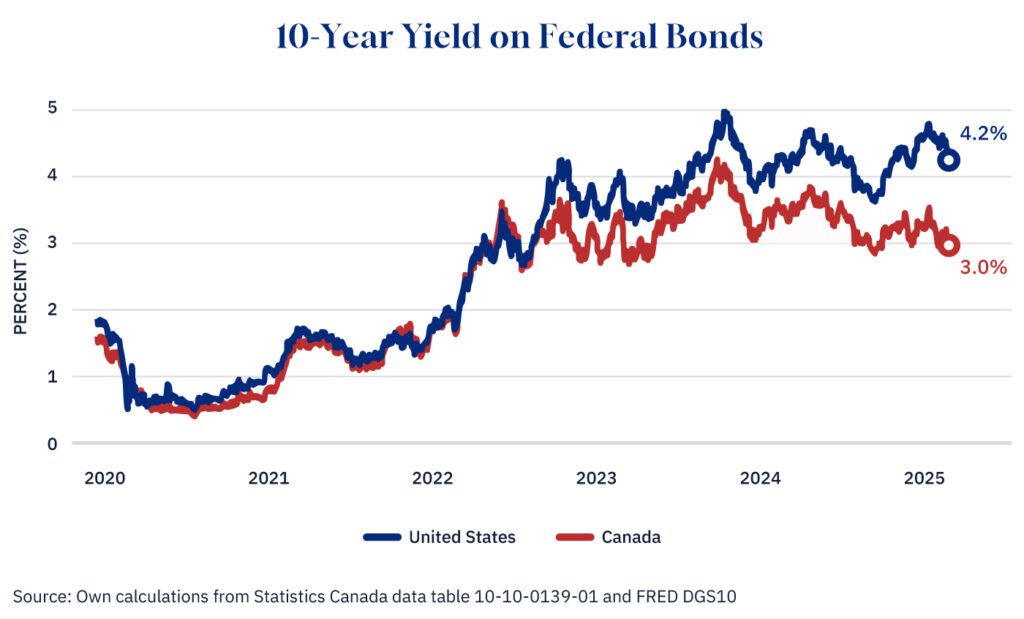

This level of borrowing has serious consequences. Not the least of which is higher borrowing costs. Right now, Canada can borrow at rates a full 1.2 percentage points lower than the U.S.—3.2 percent versus 4.2 percent.

That’s a massive gap. If U.S. borrowing costs were just one percentage point lower, it would save the equivalent of about 1 percent of GDP in interest payments—roughly $30 billion annually in Canadian terms.

And the gap is widening. On average for 2025, Canada’s borrowing rates have been nearly 1.4 percentage points lower than America’s while last year the gap was 0.9 points. The year before that in 2023 the gap was 0.6 points. In 2022, it was 0.2.

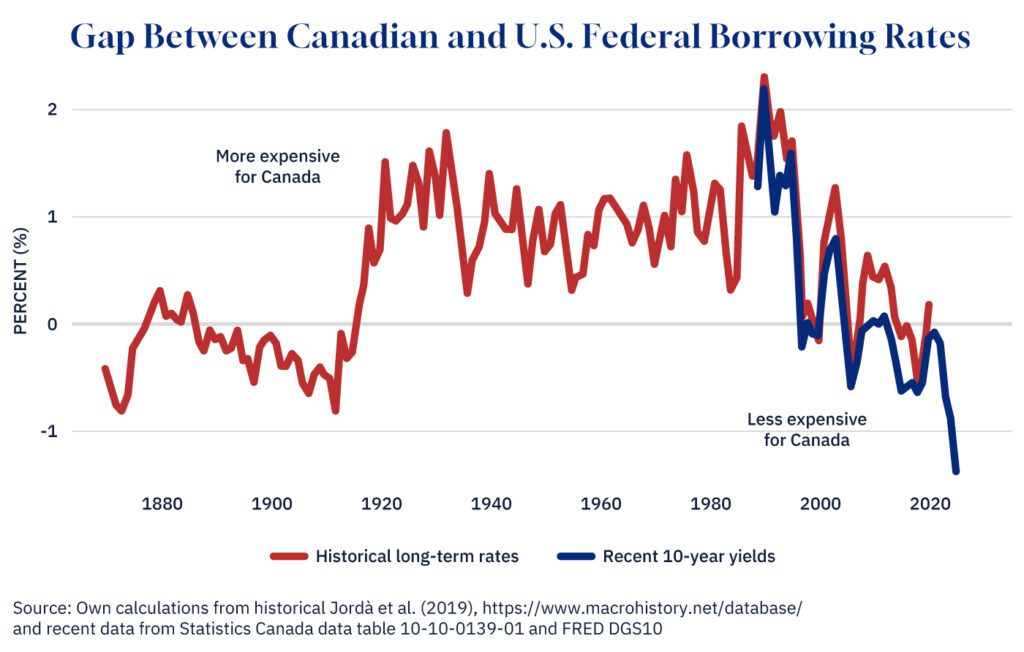

This isn’t because Canada’s fiscal position is particularly strong. It’s because the U.S. is seen as an even greater risk. Investors are demanding a premium to lend.

This is a significant reversal relative to the historical norm. Typically, Canada borrows at much higher rates than the U.S. Between the end of the First World War and the early 2000s, for example, Canada typically borrowed at a full percentage point more than the U.S. Not in recorded history (since at least 1870, that is) has the borrowing rate gap in favour of Canada ever been wider.

The situation is about to get worse for the Americans.

Last week, the U.S. House of Representatives passed a budget bill that seeks to overhaul the country’s finances. Much remains uncertain, and the bill could change significantly. “It’s sort of the kickoff in what will be a four-quarter game,” said Speaker Mike Johnson, as quoted in the New York Times. But whatever the final details, it is set to have a major impact on revenues, spending, and, most importantly, debt.

The plan includes $4.5 trillion in tax cuts, with the details yet to be determined. Spending reductions are estimated at $2 trillion, but again, the specifics remain unclear. An additional $300 billion is earmarked for border security and defence. The bill also raises the debt ceiling by $4 trillion. If spending cuts fall short, tax cuts will be reduced accordingly—an uncharacteristic development for U.S. fiscal policy. Even under the most optimistic assumptions, the net effect is to increase the 10-year deficit by roughly $3 trillion.

For context, extending the 2017 tax cuts alone is expected to cost around $4 trillion over the decade.

In practical terms, the plan would increase the deficit by roughly 0.8 percent of GDP annually. If Canada were to implement a comparable policy, that would mean adding $25 billion to the deficit each year.

Imagine a Canadian government adopting a policy to increase the deficit by the equivalent of $25 billion annually for a decade—pushing debt-to-GDP up by eight percentage points. It would be widely criticized, and rightly so.

To be clear, none of this means Canada can afford complacency. The U.S. tax cuts will create a real competitive challenge for Canada, and policymakers should respond with reforms that make our economy more attractive for investment. But Canada has another advantage it must not squander: we are not yet in the kind of crisis the U.S. is hurtling toward.

Between 1995 and 2015, successive governments—Liberal and Conservative alike—demonstrated that efficient government and sound fiscal policy were not just possible, but expected. While this has not been the case in recent years, the U.S. experience, combined with rising uncertainty in Canada’s economy, could—and should—lead Canadian governments to again prioritize a more prudent fiscal policy.