This article originally appeared in The Hub.

By Trevor Tombe, June 19, 2026

The cost of living is the number one worry for Canadians today—and it isn’t even close.

In a recent Abacus Data poll from earlier this month, fully 66 percent of Canadians surveyed cited the cost of living as a top priority. That’s nearly double the share who cited the economy, health care, or even Donald Trump as a concern.

Rising oil prices have only worsened the situation. After the U.S. attack on Iran earlier this year, oil that traded in the mid-$60s per barrel in early February shot above $110 by early April. While it has since fallen to the low-$80s as I write this, following the tentative peace deal, that is still a big jump compared to earlier this year. Gas prices are up nearly 40 percent, and over time, this could push up the price of many other goods and services too.

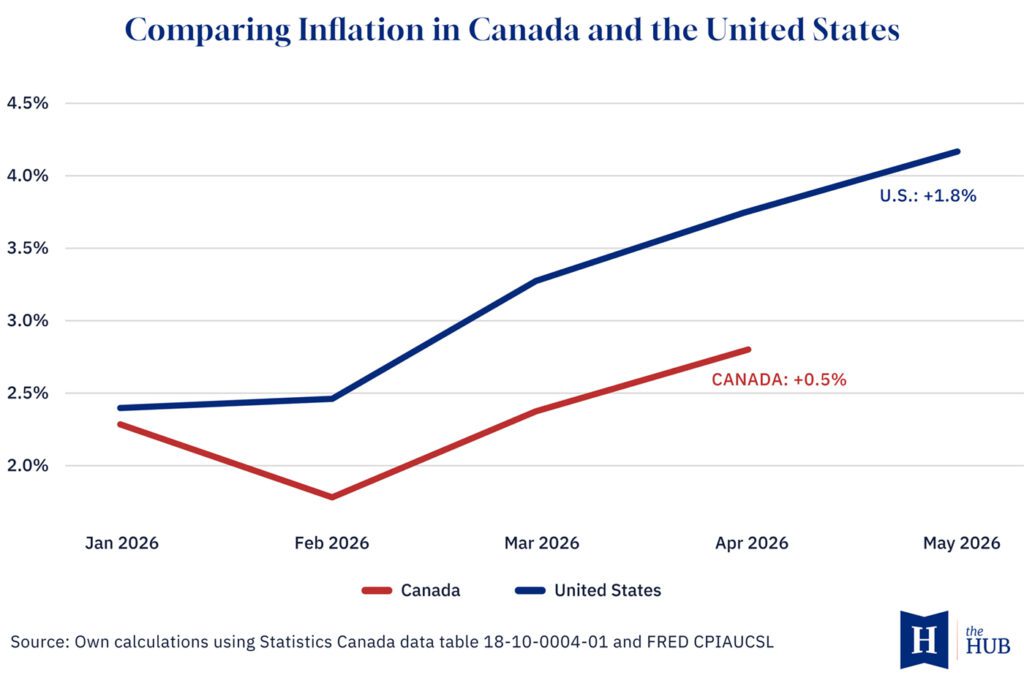

And yet inflation has not spiked. It’s up, yes, but by far less in Canada than in the U.S.

At the start of the year, Canada’s inflation rate was 2.3 percent. And in the most recent data, it sits at 2.8 percent. In the U.S., by contrast, inflation has reached 4.2 percent, the highest rate in three years, despite starting from a similar initial position in January as Canada (at 2.4 percent).

Even when Statistics Canada reports its updated measure of inflation for May next week, it still won’t be anywhere near the U.S.

So why is Canada’s inflation so much lower?

Where the gap comes from

The main reason is mundane: the two countries simply measure inflation differently.

Underlying price pressures in Canada and the United States are actually quite similar, despite the wide gap in the headline numbers. If Canada calculated inflation the way the U.S. does, as I’ll show, our rate would be a good deal higher.

Part of the gap is also policy. Ottawa suspended the excise tax on gasoline, which shielded Canadians from roughly a quarter of the increase in pump prices that would otherwise have hit. That one measure may shave about 0.2 percentage points off the May 2026 inflation rate.

But that temporary tax change aside, the drivers of inflation in both countries are quite similar.

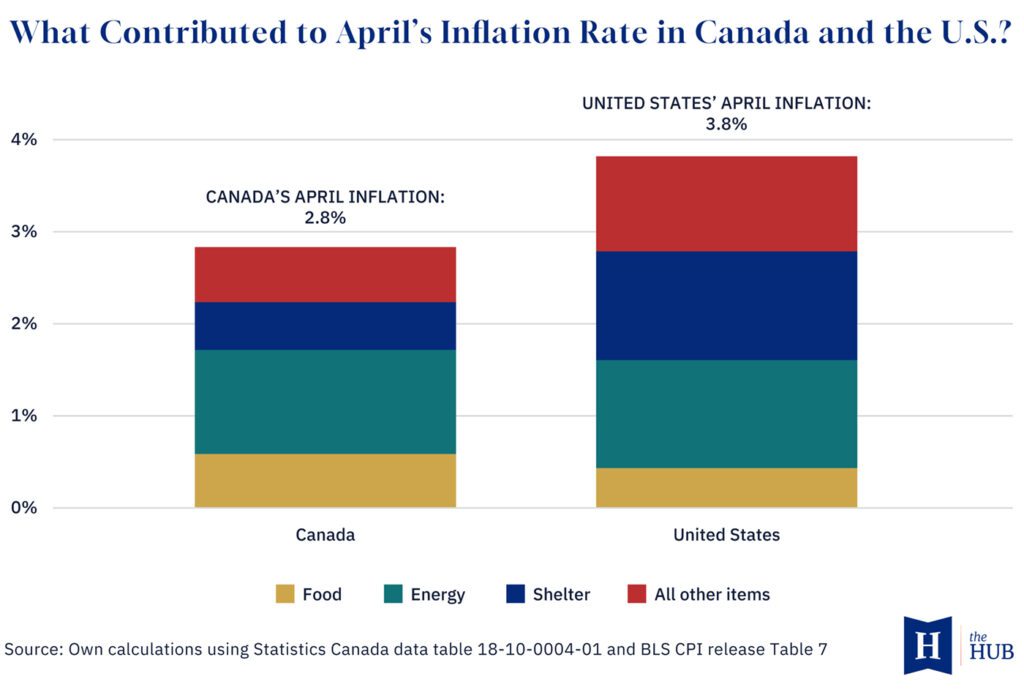

Back in April, groceries contributed 0.4 percentage points to Canada’s inflation rate. In the U.S., they contributed only 0.2 percentage points. Food overall contributed 0.6 percentage points in Canada, compared with 0.4 points in the U.S.

Energy, the big driver in both countries, contributed 1.1 percentage points to Canada’s inflation rate in April. In the U.S., it contributed 1.2 points. Again, very similar.

The big difference is shelter.

In America, shelter contributed fully 1.2 percentage points to inflation in April. In Canada, the contribution from shelter was less than half that, at 0.5 points.

It’s not that rent is rising faster there than here. Rent contributed 0.3 percentage points to inflation in Canada but contributed only 0.2 points in the U.S.

Instead, it mainly comes down to the cost of owning a home. Or at least our estimates of those costs. In the U.S., those costs added 0.9 percentage points to inflation in April, but in Canada, they barely added 0.1 points. That matters enormously, because homeownership is one of the largest items in the basket of consumer goods and services.

Why such a big difference?

How each country counts your home

In Canada, we add up several real cash costs that owners face: mortgage interest, property taxes, maintenance, insurance, and the like. We also try to capture a cost that isn’t out of pocket but is real all the same—the wear and tear on a home as it ages. That’s depreciation, or what’s called replacement cost.

The U.S. does it differently. Rather than tallying an owner’s actual costs, it asks a different question: What does it cost an owner to live in their home instead of renting it out? If you live in your home, you give up the rent you could have earned. That foregone rent is the cost. It’s called owner’s equivalent rent, and the Americans estimate it.

There is no clearly right or wrong way to do this. Each approach has pros and cons. But this difference drives nearly the entire inflation gap between the two countries.

For homeowners in the U.S., the “foregone rent” is rising because rents overall are rising, at nearly 3 percent over the past year. But for homeowners in Canada, many key components are actually falling. Mortgage interest costs are lower than they were last year. The measure of depreciation is also lower. Property taxes, insurance, and repair costs are up, but overall Canada’s measure of the cost of homeownership is up only about half a percent.

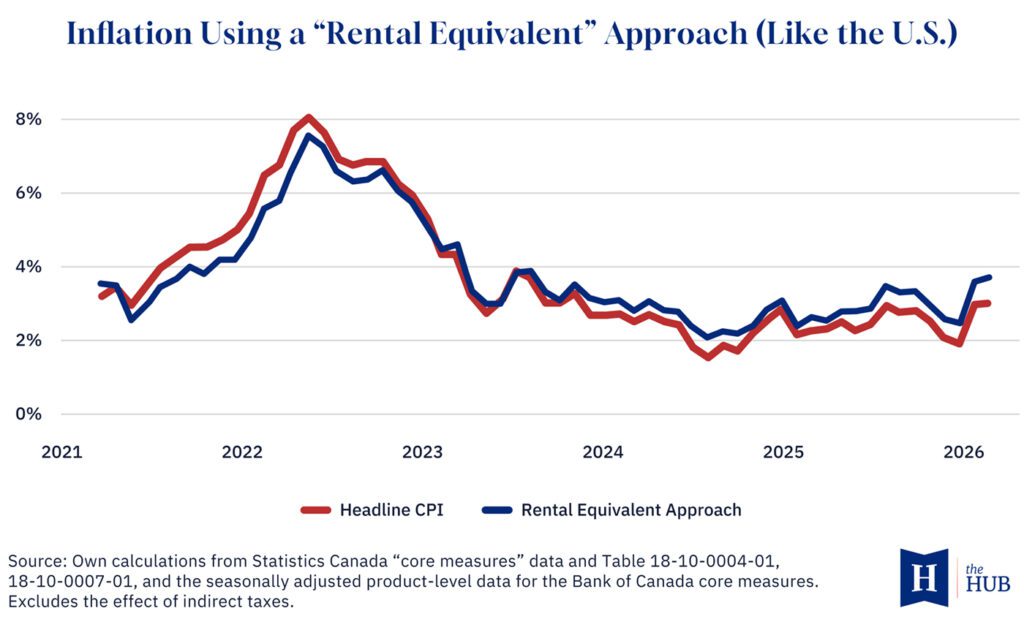

But if Canada calculated inflation in the same way as the U.S., using the so-called rental equivalence approach, I estimate that overall inflation would have been quite a bit higher in April, at roughly 3.7 percent (excluding the effect of tax changes; compared to the U.S. rate of 3.8 percent that month). And by next week, this measure could easily approach 4 percent.

So while Canada’s headline inflation rate appears well below America’s, the pressures households face are much the same. We just measure them differently. And nearly the entire difference between the two countries comes down to this one critical measurement choice around home ownership costs.

Strip that away, and the two countries look far more alike.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School of Public Policy, a Senior Fellow at the Macdonald-Laurier Institute, and a Fellow at the Public Policy Forum.