This article originally appeared in The Hub.

By Trevor Tombe, April 1, 2026

Every province in Canada is now running a deficit. And there have been several credit rating downgrades in recent weeks, including to Nova Scotia, Quebec, and British Columbia.

It’s natural to wonder if governments spend too much or tax too little. But that’s not the main problem. Our governments face a growth problem, not just a budget problem. The economy isn’t growing fast enough to support current commitments. Yet recent budgets lack bold, growth-enhancing reforms.

To see why that matters, it helps to start with the scale of our short-term fiscal challenges.

A dire budget season

In Ontario, the budget projected a deficit of nearly $14 billion, its largest since the pandemic. Quebec is no better. Its budget projects a deficit of nearly $9 billion following several years of comparably large shortfalls. Nova Scotia, New Brunswick, Saskatchewan, and Manitoba are also projecting deficits, as is Alberta (although depending on how the conflict in Iran unfolds, that may not actually come to pass). Overall, the combined value of provincial shortfalls rivals that of the federal government.

But most concerning of all is British Columbia, with a deficit of more than $13 billion for the coming year. At nearly 3 percent of its GDP, it’s the largest deficit in the country and roughly 50 percent larger than the federal government’s. It also marks the sixth consecutive deterioration in that province’s budget balance. And for every year from 2024 through 2028, the deficits exceed even that experienced during the pandemic.

The result: debt levels will exceed 37 percent of GDP within the next two years, higher than any point in its post-war history. And it puts B.C. on track to become one of the most indebted provincial governments in Canada, behind only Newfoundland and Labrador (and possibly Quebec).

Despite large current deficits, the long-term challenges are even more significant.

The problem behind the problem

Demographics, of course, will strain health-care systems across the country. That’s not news, so I won’t dwell on it here.

The deeper problem is that fiscal sustainability is, in the long run, almost entirely a question of productivity growth. And on that front, Canada has a serious problem that no budget tinkering can fix.

Allow me to illustrate. Long-term projections, whether by myself (over at Finances of the Nation), the Parliamentary Budget Office, or the federal government, all look ahead and ask what trajectory net debt levels are on, and what may be required to ensure they do not rise unsustainably over time. These projections reveal that, overall, neither federal nor provincial budgets are sustainable.

For the federal government, the required fiscal adjustment is on the order of what I estimate to be about 1.5 percent of GDP. That is equivalent to five percentage points of additional GST, taking it from 5 percent to 10. For provincial governments, the adjustment needed to maintain a stable debt trajectory over the long term is even larger, at something just shy of two percent of GDP overall and considerably higher for British Columbia.

Today’s provincial deficits are simply minor in comparison.

Why productivity changes everything

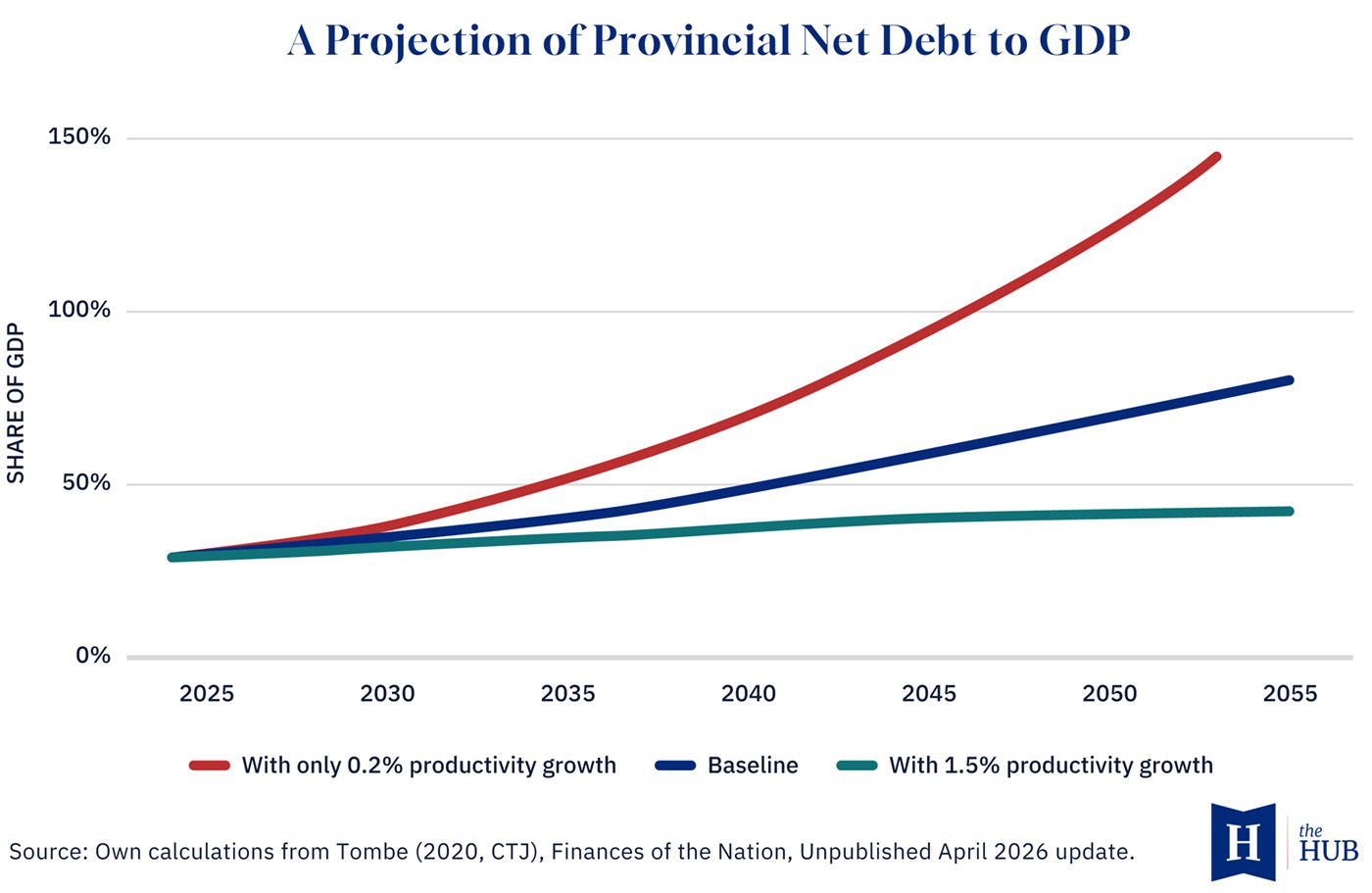

All these projections, however, rest on one important assumption: that productivity growth in Canada returns to something closer to the historical norm.

But over the past 10 years, labour productivity in Canada has grown by approximately 0.2 percent per year, whereas the average between 1995 and 2015 is over 1.3 percent. Given our recent struggles to achieve normal growth, and the lack of deeper structural reforms to move the needle, there is reason for concern.

“If productivity growth continues at the sluggish pace of the past decade, the policy adjustments needed to keep public finances sustainable would grow several-fold. Over the next 50 years, I estimate that stabilizing provincial debt would require tax increases or spending cuts amounting to about 5 percent of GDP. And a longer-term (end-of-century) projection suggests an adjustment of nearly 9 percent of GDP is needed.

That is simply not feasible to address either on the spending side or the revenue side. Even the smaller adjustment would be equivalent to increasing general sales taxes across the country by roughly 15 full percentage points (imagine the GST rising to 20 percent). On the spending side, it would be equivalent to a roughly $170 billion immediate and permanent cut.

By contrast, if productivity growth accelerates to a little above where it used to be not that long ago, then the fiscal problems of both the provincial and federal governments are, for the most part, solved.

What budgets missed

That is why the real omission from this year’s budgets was not just fiscal restraint. It was the absence of large-scale fundamental efforts to raise investment and productivity.

Tax reforms to dramatically increase investment incentives. Making capital investment immediately and fully deductible across the board, as a permanent feature of the tax code. A wholesale reform of business income taxes across provincial and federal governments, to harmonize them at lower rates, could deliver additional benefits.

Addressing tax competitiveness on the personal income tax side also matters if Canada wants to attract and retain talent in high-skilled and increasingly technologically advanced sectors. Increasing competition by eliminating barriers to entry across roughly one-fifth to one-third of Canada’s economy could also boost growth. As could enacting full and immediate automatic recognition of professional credentials across all provinces.

Today’s deficits may have legitimate short-term justifications: trade disruptions, rising uncertainty, and so on. But that short-term focus should not distract from the longer-term challenge. A return to historically normal productivity growth is not a miracle. It is the bare minimum needed to make the fiscal math work. And if we can do a little better than that, the challenge largely solves itself.

The question is whether we’re willing to do what it takes to get there.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School of Public Policy, a Senior Fellow at the Macdonald-Laurier Institute, and a Fellow at the Public Policy Forum.